Remember – Recoveries Have Rewarded Patience

|

As of yesterday, we have officially hit the 2-year anniversary of the market bottom on March 23, 2020. March 2020 was one of, if not the, most volatile months in the stock markets history. Markets were tripping circuit breakers left and right and stocks were declining at a rapid pace as we digested the impact of the COVID-19 breakout. What we have seen in the markets since this official market bottom has been nothing short of remarkable. We went from wiping our groceries down with Clorox wipes to the S&P 500 rising 102% (through this week) in just under 18-months, making it one of the greatest bull markets in the stock markets history: |

It is safe to say not many investors envisioned this remarkable turnaround. But let this serve as a reminder that recoveries in the stock market have rewarded investors who were able to stay patient. When dealing with intense volatility and uncertainty, investors can become spooked, and rightfully so.

It is safe to say not many investors envisioned this remarkable turnaround. But let this serve as a reminder that recoveries in the stock market have rewarded investors who were able to stay patient. When dealing with intense volatility and uncertainty, investors can become spooked, and rightfully so.

But if you’ve ever taken an economics course, you might remember this basic principle: Economies and financial markets, such as the stock and bond markets, move in cycles. That is, you can count on markets to experience lows, when prices fall, and peaks, when prices surge. While no one has perfected the science of knowing exactly when those lows and highs will occur, you know the financial markets (and most global economies) will eventually come back around.

Vanguard has summarized the four stages of a stock market cycle:

This emphasizes the need to maintain a diversified and balance portfolio. When you are highly concentrated in a particular company or sector, you are subject to intense downturns which may cause reactive selling.

This emphasizes the need to maintain a diversified and balance portfolio. When you are highly concentrated in a particular company or sector, you are subject to intense downturns which may cause reactive selling.

Taking the long view

When the financial markets are in turmoil and account balances start to fall, there can be a strong temptation to attempt to “do something” to stem any perceived losses. Yet it is often the case that staying the course—or doing nothing—proves to be the better path.

Here is one recent example: A hypothetical 60% stocks/40% bonds portfolio that stood at $1 million on January 1, 2020, would have lost about 20% of its value by March 23—when the stock market bottomed out from the coronavirus pandemic. Yet converting the portfolio to cash at that time would have cost an investor more than $350,000 over the next eight months versus the alternative of staying invested.

When faced with a similar situation, consider how you might feel if markets rebounded and you could have recouped all your money, and more. That’s why it’s best to stick to the long-term plan we have built together. Any changes should be made because of changes in your life, not changes in the markets. If you have questions about making portfolio moves, speak with us.

Staying the course can pay off; abandoning course can be costly

Returns for a hypothetical $1 million global portfolio consisting of 60% stocks/40% bonds

We remind our clients that staying invested can be one of the greatest decisions they can make, even if it feels uncomfortable at the time.

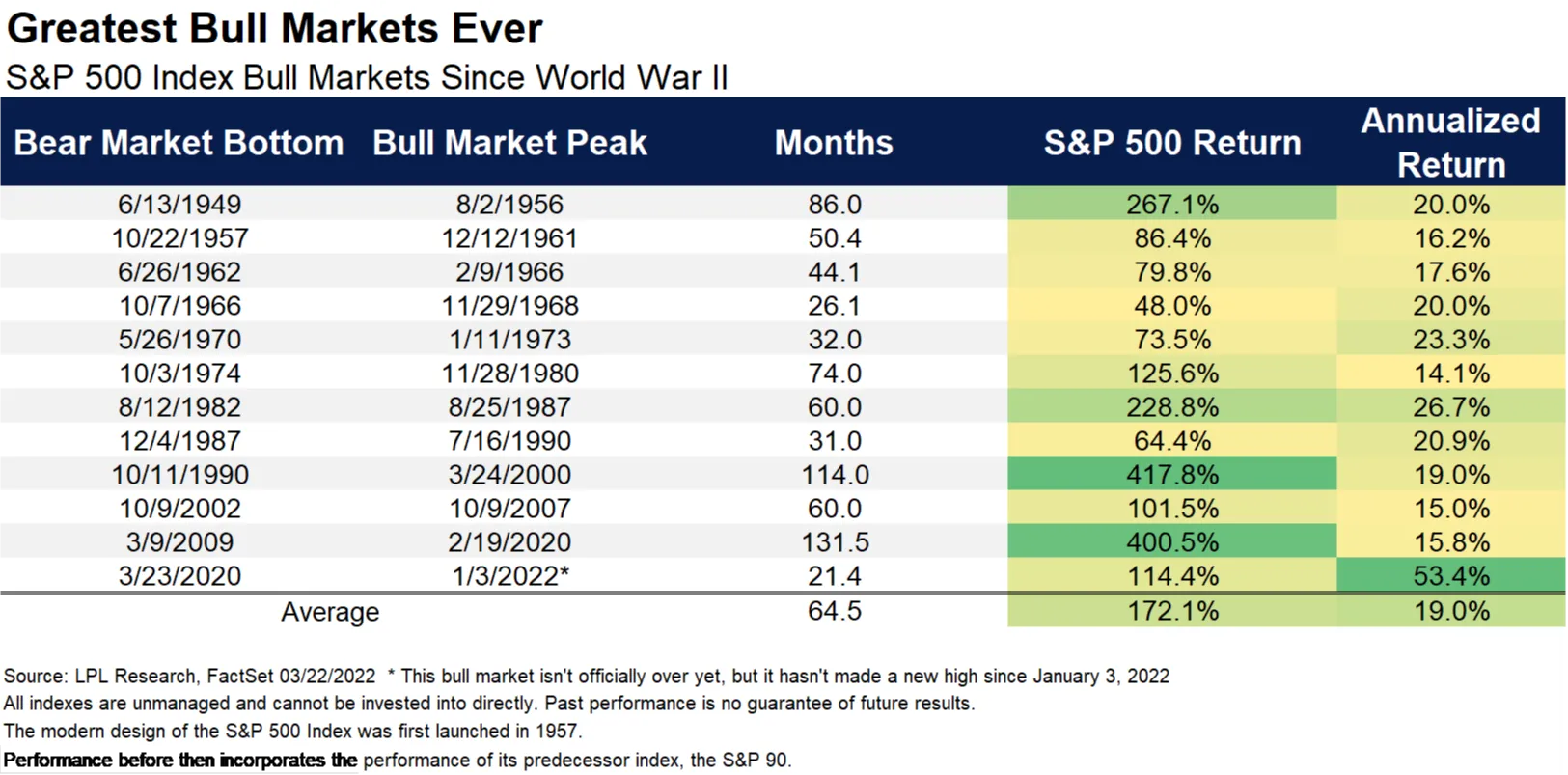

As we enter Year 3 of this bull market, lets assess the chart below which was put together by LPL Research:

While we don’t know for certain what the future holds, history shows that Year 3 is a major test for a bull market. In some years, it has marked the end of the bull market and in other years, there have been modest gains, returning 5.2% on average for the S&P 500.

While we don’t know for certain what the future holds, history shows that Year 3 is a major test for a bull market. In some years, it has marked the end of the bull market and in other years, there have been modest gains, returning 5.2% on average for the S&P 500.

As we have seen in the first 3-months of the year, Year 3 of a bull market can be bumpy. But let this serve as a reminder that history has shown if you are able to stay patient, you are typically rewarded.

Disclosure: This material is for general information only and is not intended to provide specific advice or recommendations for any individual.